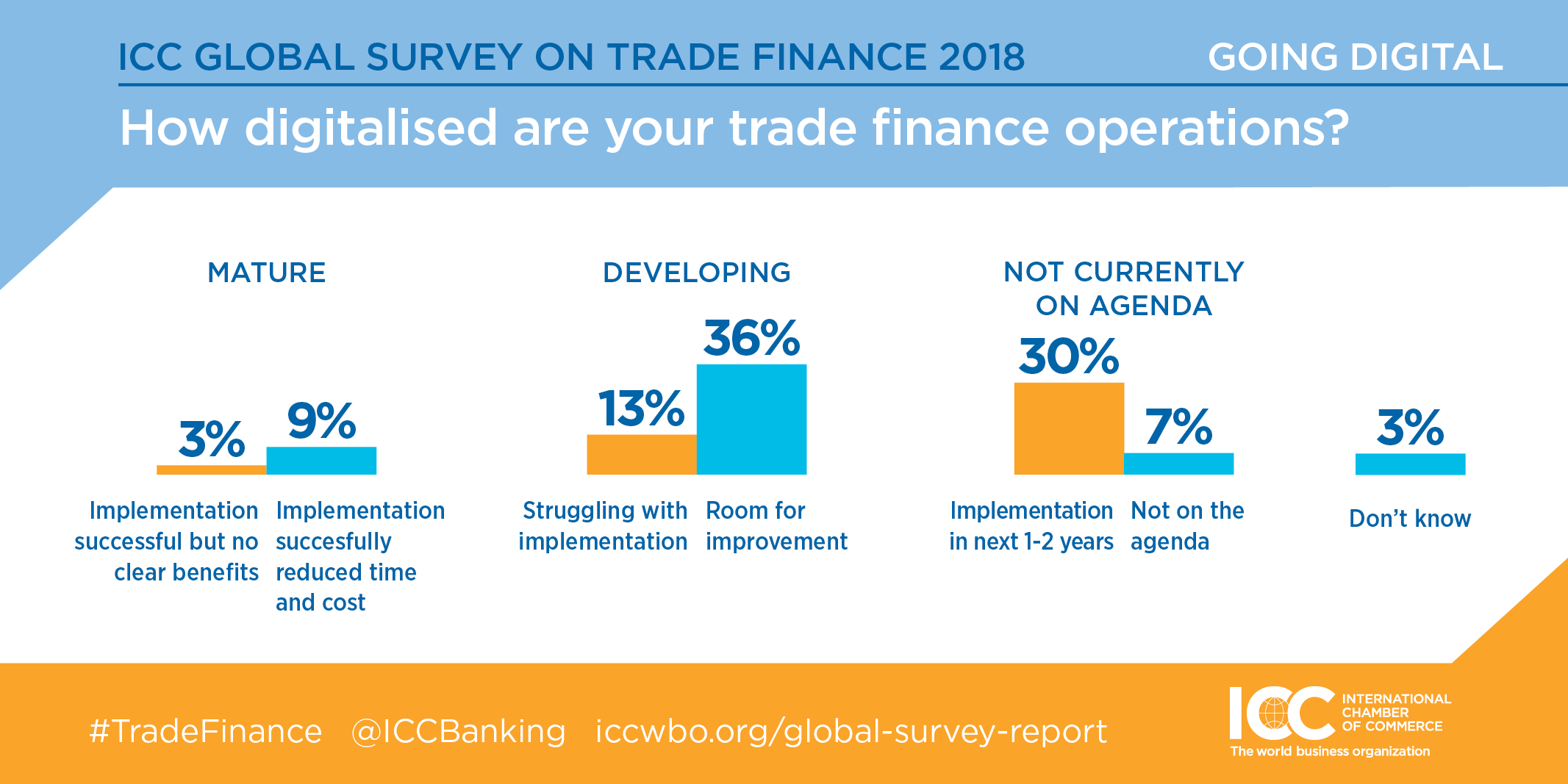

The International Chamber of Commerce’s (ICC) report says over 60 percent of banks globally have implemented or in the process of implementing technology solutions to digitalise their trade finance operations.

The 10th annual Global Survey of the ICC titled ‘Global Trade: Securing Future Growth,’ however showed that only 9 percent agreed that the solutions implemented have so far led to a reduction of time and costs in trade finance transactions and so far led to increased efficiency.

In what the report describes as a “reality check”, 30 percent of respondents say their banks remain 1-2 years away from implementing technology solutions, while 7 percent say digitalisation is not on their agenda at all.

A heavily paper-based industry with transactions worth over $9 trillion in 2017, trade finance is often noted to be ripe for digital disruption.

The multitude of documents and players (banks, customs authorities, shippers, and insurers, among others) involved in trade finance transactions, though, make it difficult for the industry to digitalise quickly.

In the findings, 65 percent of respondents say that physical paper has to some extent been removed in the issuance/advising and settlement/financing of documentary transactions.

A notable exception is the document verification process, where 52 percent of respondents say that paper has not been removed at all.

John W.H. Denton, ICC secretary general, commenting on the development, said that, “Digitalisation in the trade finance sector will boost economic growth and sustainable development. Digitalisation will make trade more inclusive.

“The ICC Global Survey gives us invaluable insight into the practical experiences and real challenges of business as we seek to take advantage of game-changing technologies and advance these broader shared goals.”

Conducted annually, the ICC Global Survey report is the world’s most authoritative review of the trade finance industry, based on exclusive information from over 250 banks in more than 90 countries.

The survey results are bolstered by contributions from an international array of leading voices on trade and finance, including experts from the World Bank, the Boston Consulting Group (BCG) and the World Trade Organization.

A single trade finance transaction can require over 100 pages of documents, with an estimated four billion pages of documents currently circulating in documentary trade. According to BCG estimates, digitalisation could cut trade finance costs by up to $6 billion in 3-5 years and boost banks’ trade finance revenues by 10 percent.

The ICC Global Survey figures demonstrate that a majority of banks are moving towards greater digitalisation, recognising its potential gains, yet only a minority have so far seen technology solutions increase their operational efficiency.

“Adapting global trade finance rules to the digital era will play a pivotal role in enabling banks to capitalise on new technologies,” said Olivier Paul, head of policy at ICC’s Banking Commission, which launched a digitalisation working group in June 2017.

“ICC rules underpin over $1 trillion of transactions each year. Now, we are working to both ensure these rules are ‘e-compatible’ and establish a set of standards to enable digital connectivity for trade finance service providers,” Paul added.

Among the many other Global Survey findings, responses show that banks are bullish on future trade finance growth trends. Nearly three-quarters of banks presented an optimistic outlook for the next 12 months, with respondents headquartered in Africa and Asia Pacific the most positive, at 89% and 81 percent respectively.

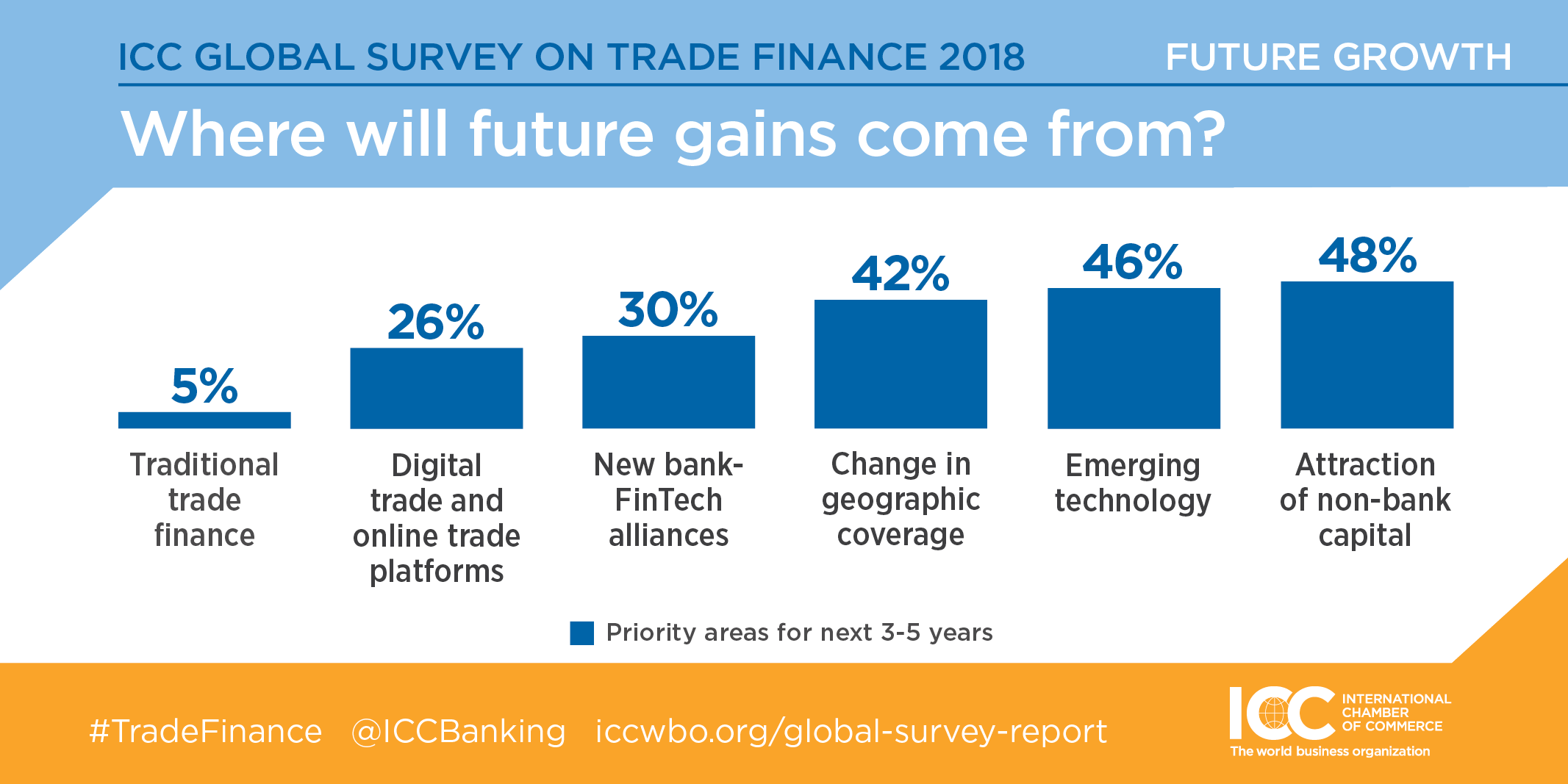

Looking ahead into the medium and longer term, only 5 percent of respondents consider traditional trade finance a strategic area of focus in the next 3-5 years. In contrast, 72 percent consider traditional trade finance a priority in the next 12 months.

Nearly half of respondents agreed that attracting non-bank capital, leveraging emerging technologies such as blockchain and shifting geographical coverage were priority areas for the next 3-5 years.

When asked what potential obstacles banks saw to their future growth prospects, respondents’ answers were stark. 93 percent of respondents named regulation and compliance as a potential obstacle while 87 percent pointed to complying with counter-terrorism and international sanctions regulation.

The ICC Banking Commission has continuously advocated for banking regulation that avoids aggravating geographical disparities in trade finance coverage, specifically across poorer regions in Africa and South Asia.

In 2017, following ICC engagement with the United Nations (UN) and national governments, the UN officially recognised the estimated $1.5 trillion trade finance gap and pledged to carry out an official review of its underlying causes.

The impact of interest rates on international trade finance pricing was also noted by the Global Survey, with 35 percent of respondents, especially large institutions, affirming that rates were driving up the cost for clients. This was particularly notable in Africa and North America where 60 percent and 54 percent reported an increase in interest rates related to trade financing.

Yet, a total of 38 percent reported maintaining the same rates, suggesting that the rise in financing costs is at least partly driven by bank-specific pricing strategies.