2023 Macroeconomic Outlook – Riding the seesaw

| What shaped the past week?

Global: Global markets traded mixed this week, as investors remained unnerved by the prospect of a global recession in 2023. In the Asian-pacific region, trading was bearish w/w, amid surprise from investors over the decision of the Bank of Japan to roll out a new bond-buying operation. The yen rose 4% against the dollar on Wednesday following the announcement.

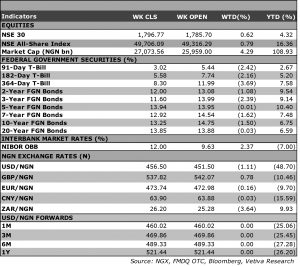

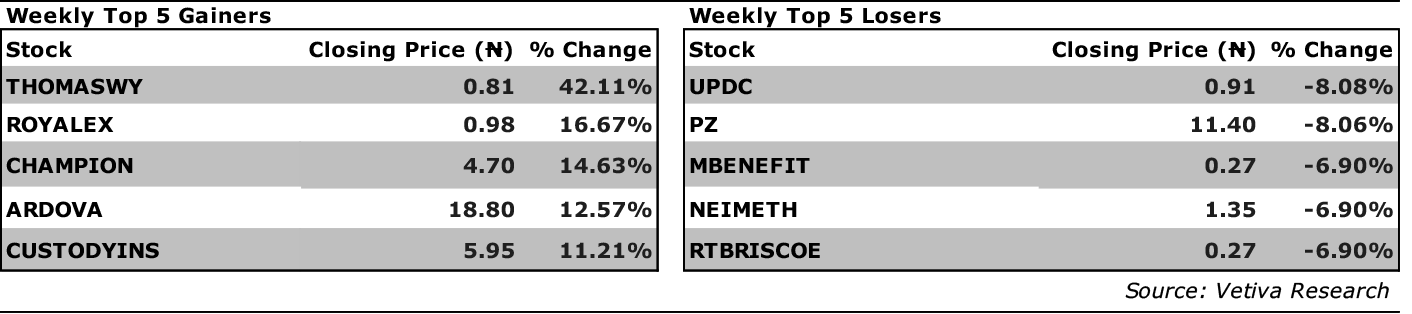

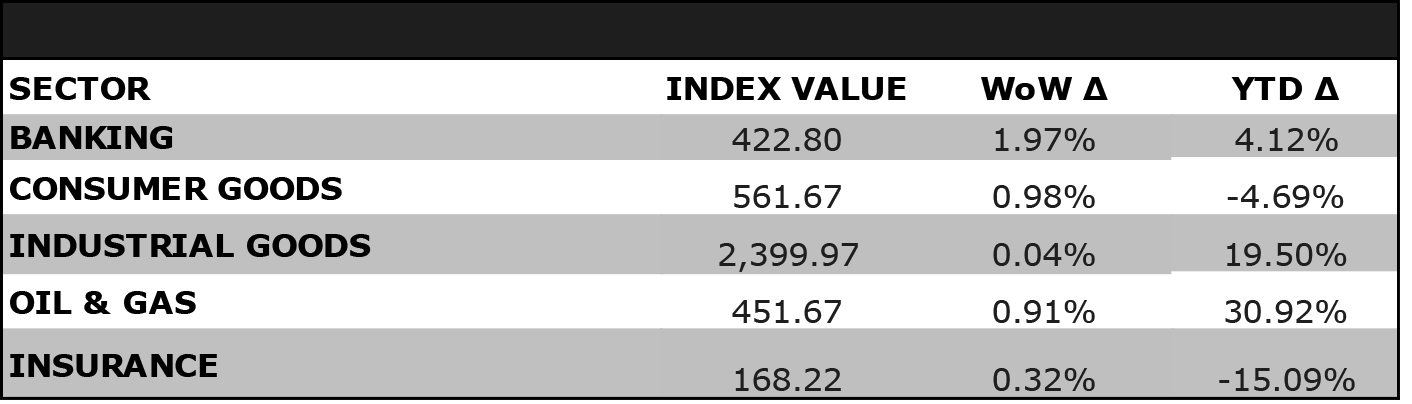

Equities: With fund managers rebalancing their portfolios as we approach the end of the year, broad-based interest across the NGX saw the index rise 0.79% w/w, to settle at 49,706pts. For a third consecutive week, the Banking sector was the best performer, rising 1.97% w/w; ZENITHBANK rose 1.87% w/w to settle at 24.55/share, while UBA and ACCESSCORP rose 2.74% and 2.37% respectively w/w. Likewise, in the Consumer Goods space, interest in low-mid cap names saw the sector rise 0.98% w/w. Moving to the Industrial Goods space, renewed interest in JBERGER (+9.91% w/w), drove the sector 0.04% higher w/w. Finally, interest in players across the oil marketing space saw the sector rise 0.91% w/w, with ARDOVA rising 12.57% w/w, driving the sector’s performance.

Fixed Income: Fixed income investors were buy-side driven w/w, as the rebalancing period for fund managers saw them pursue a wide-range of tenors across the Bonds, OMO, and NTB segments of the market. In the Bonds space, yields on benchmark bonds eased 32bps w/w on average fueled broad-based interest across the bond curve; notably, the yield on the 12.1493% FGN-JUL-2034 bond eased 85bps w/w to 13.20%. Meanwhile, in the OMO space, yields sank 541bps w/w, due to widespread interest across the OMO curve. Likewise, in the NTB space, we observed significant buy-side action over the week, as yields eased 289bps w/w.

Currency: The Naira depreciated ₦1.11 w/w at the I&E FX Window to ₦456.50.

|