November 2022 Inflation – Year-long fuel scarcity intensifies inflation in November

| What shaped the past week?

Global: Global markets traded in a bearish manner this week, as investors remain unnerved over the possibilities of a global recession. Investor focus shifted to the latest policy meetings from key central banks, where we saw another round of rate hikes from monetary officials. Starting in the Asian-Pacific region, where the focus was on the latest batch of economic data out of the region, China saw retail sales fall 5.9% y/y, while industrial production came in at 2% y/y, however both data prints were below market expectations; for the week, the Shanghai Composite lost 1.22% w/w, with the Nikkei-225 and ASX falling 1.34% and 0.89% w/w respectively.

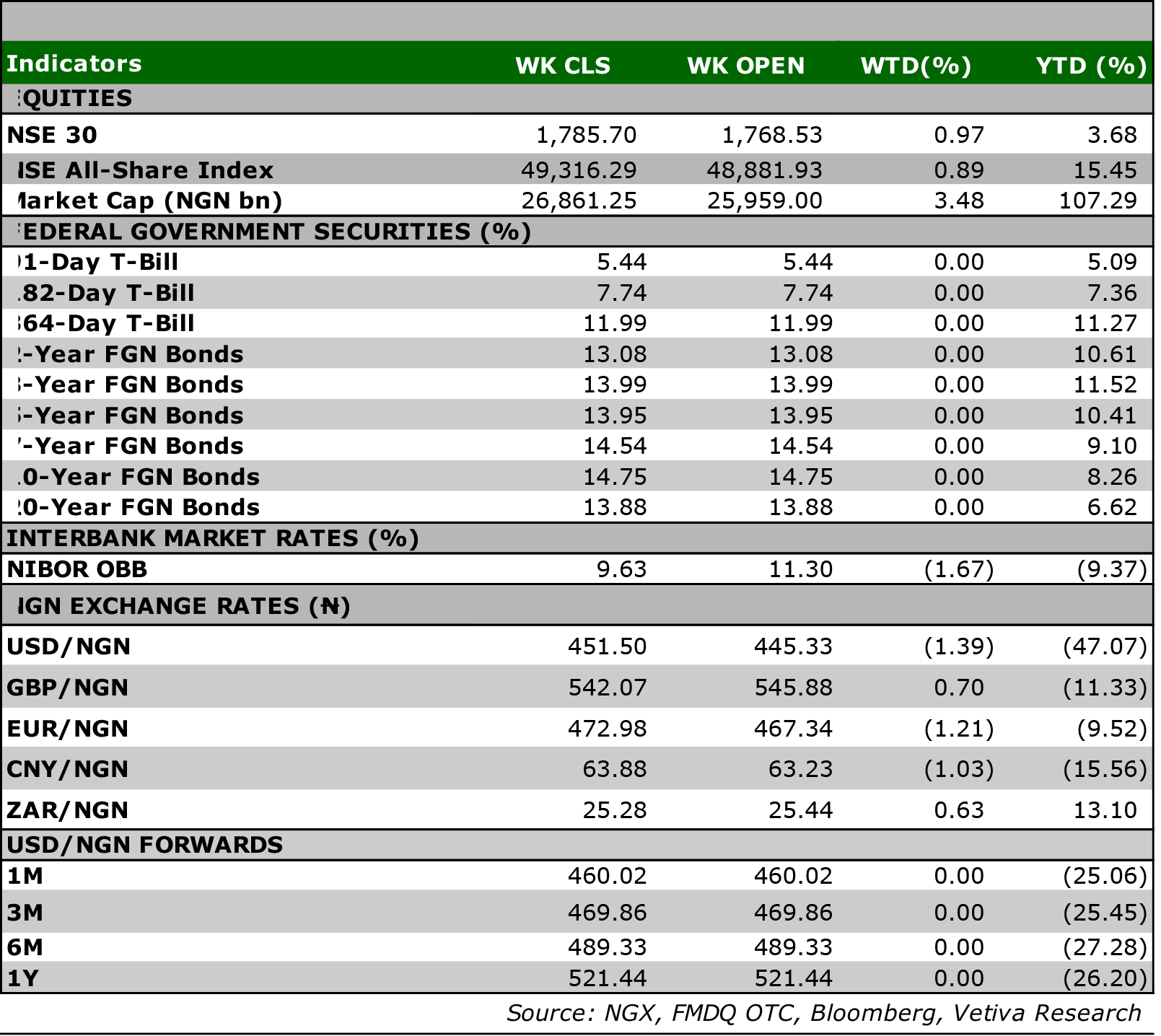

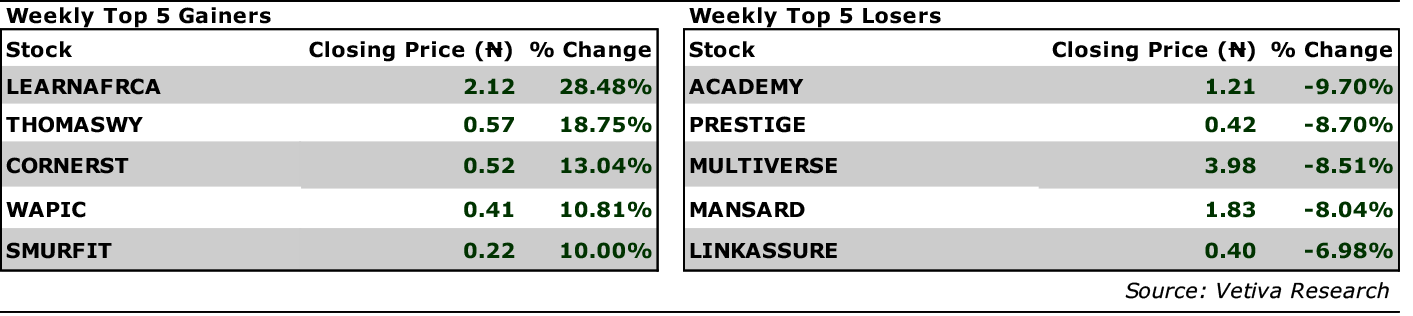

Equities: Investors were largely bullish across the equities market, as the NGXASI rose 89bps w/w to close at 49316.29pts. Banking stocks were the best performers for the week, as the sector gained 287bps w/w; of note, ZENITHBANK led the way, as the counter soared 905bps w/w; additionally, we saw interest in FIDELITYBK, which gained 241bps w/w. Likewise, in the Industrial Goods space BUACEMENT recorded another strong performance, rising 660bps w/w, fueling the 343bps w/w return for the Industrial Goods sector. Finally, interest the oil marketing space saw the Oil and Gas sector rise 0.36% w/w; ARDOVA was the top performing counter, rising 951bps w/w. On the other hand, investors turned bearish on the Consumer Goods space, as the sector lost 20bps w/w, dragged by profit-taking action in DANGSUGAR (-432bps w/w).

Fixed Income: On Monday, the Debt Management Office offered ₦225 billion and sold ₦264.51 billion across the 5-Year, 10-Year, and 15-Year tenors at stop rates of 14.60%, 14.75%, and 15.80% (Previous: 14.75%, 15.20%, 16.20%). As a result, of lower stop rates offered we saw aggressive buy-side action from investors over the course of the week, as the yield on benchmark bonds declined 63bps w/w on average. Meanwhile, it was a flat close across the NTB and OMO segments due to relatively tight system liquidity.

|

Currency: The Naira depreciated ₦1.46 w/w at the I&E FX Window to ₦451.50.

| What will shape markets in the coming week?

Equity market: It was another good week for the banking sector, in terms of both performance and activity. While, we expect some profit taking next week, we anticipate another positive week on week close on the back of positive activity in some of the heavy weights.

Fixed Income: Given the aggressive buy-side activity witnessed this week, we cannot rule out the possibility of profit-taking action from investors to start next week. Meanwhile, we expect liquidity levels to dictate activity in the NTB space.

November 2022 Inflation – Year-long fuel scarcity intensifies inflation in November Consumer prices punched higher in November to 21.47% y/y (Oct’22: 21.09% y/y). On a month-on-month basis, headline inflation rose to 1.39% m/m, 15bps higher than the previous month amid prolonged fuel scarcity and demand frontload ahead of the festive season.

Demand frontload keeps food inflation elevated Despite being at the crux of harvest, food prices rose at a faster pace of 1.40% m/m (Oct’22: 1.23% m/m). When annualised, food inflation rose to 24.13% y/y (Oct’22: 23.72% y/y). This uptick was driven by processed foods (+66bps to 1.63% m/m) and non-alcoholic beverages (+17bps to 1.39% m/m), which implies demand pressures ahead of the festive season. Surprisingly, the prices of farm products witnessed a 0.13% m/m deflation, as supply glut from year-end harvest moderated farmgate prices, showing that the impact of floods on farmgate prices was muted. Bread and cereals remained the food items with the highest price changes. This was due to a substantial reduction in wheat import from Russia amid the enforcement of sanctions against the Eurasian country.

Fuel scarcity stokes core inflation Elsewhere, core inflation, which excludes volatile agricultural produce, increased to 18.24% y/y (Oct’22: 17.76%), due to higher energy prices and exchange rate pressures. On a month-on-month basis, the core index accelerated to a 6-month high of 1.67% m/m (Oct’22: 0.93% m/m), driven by prolonged fuel scarcity in the month of November.

Consumer prices could be ready for an inflex |

While fuel scarcity has lingered in December, we have observed reduced month-on-month upticks since August, partly supported by the harvest season. Thus, we expect headline inflation to slow to 20.99% y/y in December. We attribute this decline to high base effects from the prior year and robust year-end harvest, despite factoring elevated year-end demand and fuel scarcity aftereffects. We expect reduced exchange rate volatility to keep core inflation in check despite higher outturns. Tying this together, we now expect headline inflation to average 18.73% y/y in 2022 (2021: 16.98% y/y).